OKX Ceases Operations in India, Citing Regulatory Hurdles

03/21/2024 21:47

OKX has emailed its users in India to inform them that it will discontinue its services there, urging them to withdraw their funds.

Last updated: | 2 min read

Cryptocurrency exchange OKX has emailed its users in India to inform them that it will discontinue its services there, urging them to withdraw their funds by the end of April.

OKX was among the nine foreign crypto exchanges blocked in India after the local regulators issued compliance notices.

OKX Shuts Down Services In India

In a notice sent to Indian users on Thursday, March 21, OKX urged its customers to close their accounts and redeem funds before April 30.

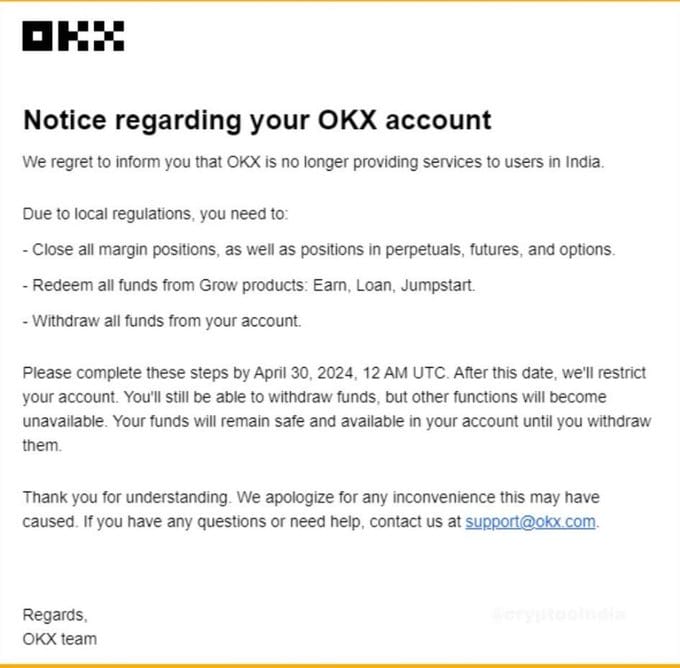

To justify the action, the CEX cited local regulatory hurdles as the primary reason behind the decision. The notice stated, “We regret to inform you that OKX is no longer providing services to users in India.”

As a result, OKX users in India were instructed to close all margin positions, perpetuals, futures, and options and redeem funds from products like Earn, Loan, and Jumpstart before the April 30 deadline at midnight.

Furthermore, OKX customers are also advised to expedite the withdrawal of their funds before the deadline to avoid any losses. Moreover, the OKX exchange assures users that their funds will remain safe and available until withdrawn. This decision came after the FIU requested that the Ministry of Electronics and Information Technology block the websites of the notified crypto exchanges within two weeks; OKX faced website and application blocks in January.

Despite attempting to comply by applying for a new registration process with stringent Know Your Customer checks following a block on its website and application in January, OKX’s notice suggests that it could not successfully complete the registration process.

On December 28, 2023, India’s Ministry of Finance’s Financial Intelligence Unit (FIU) issued notices to several cryptocurrency exchanges, including Binance, Huobi, Kraken, Gate.io, KuCoin, Bitstamp, MEXC Global, Bittrex, and Bitfinex, for operating unlawfully within the country.

The FIU directive mandated that any exchange serving Indian users register as a “reporting entity” and submit statements to the income tax department. Failure to comply resulted in recommendations for the Ministry of Electronics and Information Technology to block these exchanges’ websites.

Regulatory Uncertainty Persists for Cryptocurrency Exchanges in India

On December 28, 2023, the FIU served notices of noncompliance to several exchanges, including Binance, Kraken, Huobi, and Gate.io, aimed at gathering financial intelligence under the Prevention of Money Laundering Act.

Notably, OKX was not named in the public statement. While some local exchanges, such as CoinSwitch and CoinDCX, complied with the FIU’s requirements, numerous international exchanges failed to adhere to Indian law, as stated by the FIU.

Subsequently, Apple’s App Store and Google Play Store in India blocked apps from Binance, KuCoin, Bitget, Huobi, OKX, Gate.io, and MEXC crypto exchanges weeks after the Indian government issued the noncompliance notice.

Navigating the cryptocurrency landscape in India remains challenging for foreign exchanges, primarily due to the absence of clear regulatory guidelines and stringent government actions.

Despite ongoing discussions spanning nearly four years, the Indian government has yet to outline a formal regulatory framework for the burgeoning crypto market. This lack of clarity has left industry players uncertain about their legal standing and obligations within the country.

Compounding the issue, the Indian tax regime imposes a hefty 30% tax on crypto income without provisions for offsetting losses, along with a 1% tax deducted at source (TDS) on each crypto transaction. These stringent tax regulations have prompted several established players to relocate their operations elsewhere.